The proportion of past due B2B invoices in Sweden has sharply increased from 26.7% in 2017 to 34.0%. Foreign B2B customers had a much higher default rate.

2018 brought many changes for Sweden: there was a steep increase in overdue B2B invoices, a higher average DSO and it took survey respondents in the country longer to convert B2B receivables into cash. The proportion of uncollectable B2B receivables increased slightly and bankruptcy remains the main reason for write-offs. Construction and consumer durables are problematic sectors and further deterioration of payment behaviour is likely to occur over the coming 12 months.

Creditworthy customers receive credit terms

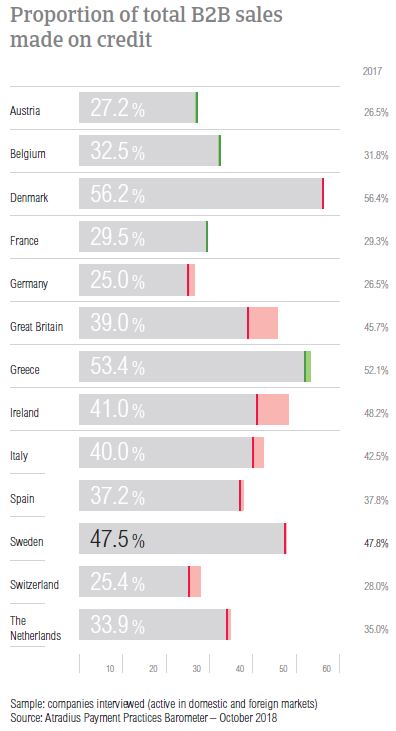

The proportion of total B2B sales made on credit in Sweden is stable at 47.5% (47.8% in 2017). This is a higher proportion of sales on credit than the 37.4% average for the region overall. Like in most Western European countries surveyed, there is a greater preference to sell on credit domestically than internationally (50.7% of domestic B2B sales on credit versus 44.2% of foreign B2B sales on credit).

The top reason why Swedish suppliers trade on credit with their domestic B2B customers is, it is a common practice in the industries in which they operate. The second most frequently mentioned reason for trading on credit domestically is the good relationship developed with B2B customers who have proven their creditworthiness and ask for credit terms. When confronted with insufficient information about the customer’s business or payment performance (20.7%), poor payment behaviour (10.3%) or high economic or political risk (10.3%), Swedish suppliers do not sell on credit.

We grant trade on credit with our domestic B2B customers because they are creditworthy and require credit.

The main reasons why Swedish suppliers trade on credit with B2B customers abroad mirror the ones cited with domestic B2B customers – credit sales are considered standard practice and a good business relationship with trusted customers. Top reasons for refraining from offering credit sales are the lack of information on the customer’s business or payment performance (mentioned by 42.4% of respondents) and high economic or political risk in the customer’s country (21.2%).

Trading on credit is the usual practice in our industry.

Late payment on the rise

In 2018, the percentage of respondents who reported late payment by B2B customers went up by 10% and it now stands at 86.2%. This is one of the biggest changes in the region, and Sweden’s percentage of respondents experiencing late payment is slightly lower than that registered in Western Europe overall. Swedish suppliers reported payment delays from domestic B2B customers almost as often as from foreign B2B customers (85.9% versus 86.4%).

The proportion of past due B2B invoices in Sweden has sharply increased from 26.7% in 2017 to 34.0% this year. Despite this being one of the biggest changes, it remains the lowest in the region, far below the regional average of 41.8%. Foreign B2B customers had a much higher default rate than domestic B2B customers.

In 2017, the average Days Sales Outstanding (DSO) figure in Sweden dropped to 30 days. This year, it is back at the level recorded in 2016, 34 days on average. Even after the increase, Sweden’s average DSO is 10 days lower than the regional average. Looking at the coming 12 months, 65.2% of respondents do not expect further changes. 20.1% mentioned that they expect another increase and 14.7% foresee a decrease.

Increase in payment delays, longer payment duration

In 2018, suppliers in Sweden gave shorter payment terms to their B2B customers (on average, 26 days). Compared to 2017, this is a one-day decrease for domestic B2B customers and a three days decrease for foreign B2B customers.

Confirming the above, 48.5% of Swedish respondents said that they usually do not differentiate payment terms between domestic and foreign B2B customers. 30.6% said that they are likely to give their domestic B2B customers less time to settle payments and 20.9% said that they would give these longer payment terms. The main reasons for differentiating payment terms in Sweden are industry practices, internal policies and the economic situation in the customer’s country.

In 2018, Swedish respondents experienced increased payment delays from their B2B customers. Domestic B2B customers delayed their payments on average by 14 days (four days longer than in 2017) while foreign B2B customers delayed payments by 22 days (nine days longer than in 2017).

The changes in payment terms and payment delays caused a significant increase in the average payment duration. This stands at 45 days and is five days longer than one year ago. Despite the increase, Sweden still has one of the fastest payment durations in Western Europe.

Based on our survey findings, the main reasons for domestic payment delays in Sweden are insufficient availability of funds (mentioned by 43.0% of respondents), buyers using outstanding invoices as a form of financing (26.5%) and the complexity of the payment procedure (25.6%). In comparison to 2017, an increased percentage of respondents reported the first and third reasons. In regards to foreign B2B customers, suppliers in Sweden reported that payments are most often delayed because of the complexity of the payment procedure (reported by 32.2% of respondents) and insufficient availability of funds (31.1% of respondents). An increased percentage of respondents reported these key payment delay factors in 2018.

53.3% of Swedish respondents said that their businesses have not been affected by overdue B2B invoices over the past 12 months. Of the remaining 46.7%, 14.8% stated that they had to pursue additional financing to manage the impact of late payment. 13.2% of respondents said that they had to default on payments to their own suppliers and 8.2% lost revenue because of past due invoices.

75% of Swedish respondents use electronic invoices

In Sweden, suppliers are mostly invoicing their B2B customers online. 75.1% stated that they are already using this method while another 6.8% want to make the move to the online environment this year. 17.1% of suppliers in Sweden said that they are not using electronic invoices and a low 1.0% that they have stopped e-invoicing.

After invoicing their B2B customers online, 53.0% of Swedish respondents received payments on invoices faster. In contrast, 4.0% reported a slowdown in payment. For 43.1% of respondents, electronic invoices did not have a noteworthy effect on payment duration.

US protectionism seen as the most significant potential risk

Like most of their peers in Western Europe, respondents in Sweden perceive US protectionism turning into a trade war as the most significant potential risk to global trade (more significant than misguided Fed policy, China’s ‘hard’ landing and geopolitical risk). The 54.2% of respondents citing this in Sweden is one of the highest percentages in the region, after those registered in Denmark and Germany. Moreover, Sweden’s percentage of suppliers seeing US protectionism as the most significant potential threat is far above the regional average (44.8%). 16.4% of respondents ranked China’s ‘hard landing’ as the most significant risk. This was the second most significant potential risk by suppliers in the country.

Increase in uncollectable B2B receivables

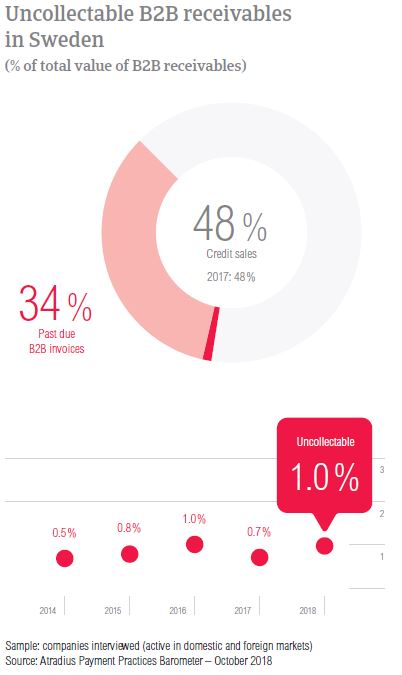

Respondents in Sweden reported that the proportion of uncollectable receivables has gone up from 0.7% in 2017 to 1.0% in 2018. Despite the increase, it is still below the regional average. Similarly to what was observed in past surveys, domestic B2B receivables were written off as uncollectable more than twice as often as foreign B2B receivables (0.7% versus 0.3%).

In Sweden, uncollectable receivables originated most often from the construction, consumer durables, electronics, business services and services sectors. The main reason why B2B receivables were uncollectable was bankruptcy. 50.0% of respondents stated this reason, a decreased percentage compared to 2017 (60.0%). Other main reasons for write-offs were the old age of the debt (mentioned by 27.4% of respondents) and the high cost of pursuing the debtors (26.2%).

Deterioration expected in the construction sector

In 2018, the average payment term given by Swedish respondents is 26 days. This is one of the shortest in the region. By sector, B2B customers in the construction and machines sectors were given the longest payment terms (on average 33 and 32 days respectively). B2B customers in the paper industry and those in the textiles sector were asked to settle their invoices the fastest (within 13 and 14 days respectively).

In 2018, B2B customers in the construction and consumer durables sectors generated some of the longest delays. Based on our survey findings, customers in these sectors paid, on average 22 days and 23 days late. Differently than what was stated in the country overall, the main reason for payment delays in the construction sector was incorrect information on invoices (mentioned by a high 41.0% of suppliers). The main reason for payment delays in the consumer durables industry was buyers using outstanding invoices as a form of financing (cited by 43.0% of respondents).

47.0% of respondents in the construction sector and 49.0% in the consumer durables sector said that they do not foresee any changes in the payment behaviour of their B2B customers over the next 12 months. Of those who expect changes, higher percentages of respondents pointed to deterioration than improvement. More specifically, in the construction industry, 37.0% of respondents foresee worsening in the payment behaviour of their B2B customers and only 15.0% improvement. 26.0% of suppliers in the consumer durables sector expect deterioration and 26.0% improvement.