As seen in France, more respondents in Belgium (30%) than in Western Europe (22.4%) expect deterioration in their DSO over the next 12 months.

Key survey results

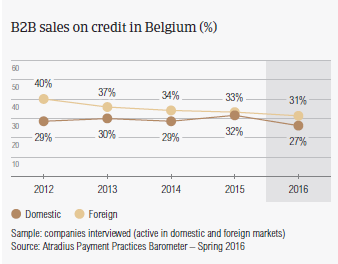

Sales on credit terms

Respondents in Belgium, like those in France, Austria, Switzerland and Germany, appear to have a quite strong aversion to granting trade credit to business-to-business (B2B) customers.

On average, nearly 30.0% of the total value of respondents’ B2B sales were transacted on credit terms. This is well below the 41.2% average for Western Europe. Compared to last year, the average value of B2B credit-based sales in Belgium decreased by around 3% (in Western Europe it remained stable). Belgian respondents’ more prudent approach to the use of trade credit in B2B transactions may reflect a challenging insolvency environment in which they currently operate (the insolvency rate in Belgium is around 2% and at a higher level than in 2007). No clear preference for selling on credit to either domestic or foreign B2B customers is shown by Belgian respondents.

30.7% and 27.3% of the total value of domestic and foreign B2B sales respectively were made on credit (survey averages: 44.8% domestic and 37.7% foreign). This reflects an almost uniform perception of payment risk arising from domestic and foreign B2B trade. This is common to the majority of the countries surveyed, except for those in Southern Europe (Greece, Italy, Spain), which seem to be notably more trade credit friendly to domestic than to foreign B2B customers.

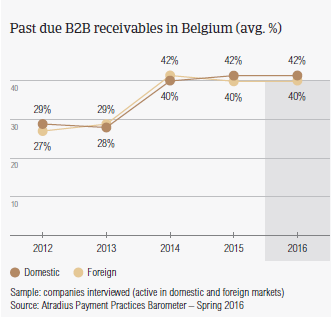

Overdue B2B invoices (%)

In line with the survey average, 92.0% of Belgian respondents experienced late payment of invoices by B2B customers over the past year. This resulted in an average of nearly 41.3% of the total value of B2B receivables remaining unpaid past the due date. This is consistent with the survey average. Late payment of invoices occurred almost equally as often with domestic customers as it did with foreign customers, and did not vary significantly over the past year. This finding tallies with the challenging business conditions Belgian businesses are currently confronted with.

Late payment of invoices (domestic and foreign) is reflected in the Days Sales Outstanding (DSO) figure posted by respondents in Belgium. This averages 51 days (survey average: 48 days), and is nine days longer than one year ago. This means that respondents in Belgium have to wait longer for cash, which is tied up in receivables, to be available to use to grow the business. Moreover, 30.0% of respondents expect their DSO to deteriorate over the next 12 months.

This may explain why more respondents in Belgium (11.3%) then in Western Europe (8.6%) consider efficiency in receivables management to be the greatest challenge to business profitability this year. This along with maintaining adequate cash flow levels (18.0% of respondents, compared to 16.4% in Western Europe) are the two most noted challenges to business profitability.

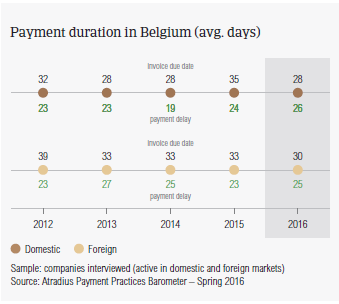

Payment duration (average days)

Payment terms extended to B2B customers by respondents in Belgium average around 29 days from the invoice date, and are consistent with the survey average (31 days). Domestic and foreign terms differ by only two days, reflecting the already mentioned uniform perception of payment risk arising from either domestic or foreign B2B trade. Compared to last year, Belgian respondents have granted much shorter payment terms to their B2B customers, particularly on the domestic market. Here average payment terms are around one week shorter than in 2015.

Despite the attempt to offset payment delays by shortening payment terms, Belgian respondents have now to wait longer than last year to receive payment of past due B2B invoices. These are settled by domestic and foreign B2B customers, on average, within 25 days past the due date (survey average: 22 days). This means that it currently takes respondents in Belgium an average of around 54 days from invoicing to turn past due B2B invoices into cash. This is almost in line with the survey average.

Key payment delay factors

In Belgium, notably more respondents (58.2%, in line with the survey average) than last year (50.3%) reported that domestic B2B customers pay invoices late due to liquidity issues. The second most often mentioned reasons for late payment by domestic B2B customers are formal insolvency of the buyer and customers’ intentional use of outstanding invoices for financial advantage (23.3% of respondents alike).

Similarly, late payment of foreign invoices due to liquidity issues was reported more often (42.6% of Belgian respondents) than last year (37.3%). However, as previously observed one year ago, for a sizeable percentage of respondents (23.0%) payment of foreign invoices is very often due to external factors which are independent of the financial stability of the customer, such as the complexity of cross-border payment procedures and inefficiencies of the banking system. This appears to heavily impact payment timing of foreign invoices in Belgium.

No matter why customers paid invoices late, this had an adverse impact on businesses surveyed in Belgium. 25.4% had to delay payments to their own suppliers, and nearly 20.0% recorded a loss in revenues. This may explain why notably more respondents in Belgium (45.7%) than in Western Europe (34.8%) plan on checking customers’ creditworthiness more often in 2016. In addition an increase in the use of risk free payment methods in B2B trade was reported by more respondents in Belgium (32.0%) than in Western Europe ( 26.0%) overall.

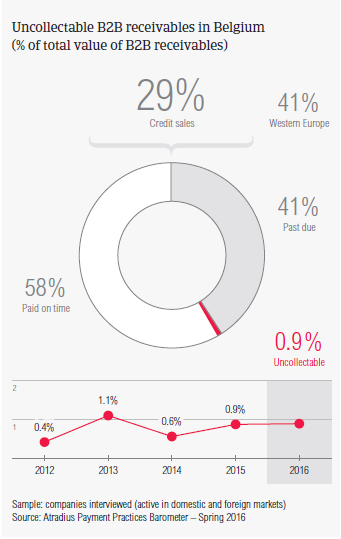

Uncollectable receivables

The proportion of B2B receivables reported by Belgian respondents as being written off as uncollectable (less than 1% of the total value of B2B receivables) is lower than the average for Western Europe (1.3%).

Domestic uncollectable receivables were written off almost as often as foreign ones. Uncollectable domestic B2B receivables originate most often from the construction, consumer durables and services industries.

For most of the respondents in Belgium (55.2%) B2B receivables were uncollectable mainly due to the customer being bankrupt or out of business (respondents in Western Europe: 59.3%). At the same time, around 25.0% of respondents in the country reported that write-offs were mainly due to the failure of collection attempts, and because the additional costs to pursue the trade debtors was greater than the value of the receivable itself.

For more insights into the B2B receivables collections practices worldwide, please see the Global Collections Review by Atradius Collections (free download after registration), available from October 2016 on www. atradiuscollections.com.

Payment practices by industry

Survey respondents in Belgium reported granting trade credit terms mainly to B2B customers in the consumer durables, construction, and services industries. Invoice payment terms extended by Belgian respondents to their B2B customers in the financial services industry are above the country average (averaging 32 days from invoicing). B2B customers in the construction industry settle past due payments the slowest (slightly above the average for the country).

The construction industry generated an above average (for the country) proportion of overdue invoices. However, according to most of the respondents in Belgium (68%), late payment of invoices due to liquidity constraints from customers occurred most often in the consumer durables industry. On the contrary, late payment in the construction industry most often resulted from the formal insolvency of the customer (35.0% of respondents).

Most of the respondents in Belgium expect payment practices of B2B customers in the consumer durables industry to deteriorate slightly over the next 12 months. No significant change is anticipated in respect to payment practices of customers in other industries.

Documentos relacionados

3.82MB PDF